Mark Smith

Mark Smith

What is a liquidator?

A liquidator is a person appointed, in the winding up of a corporation, to assume control of the company's affairs and to discharge its liabilities...

ATO kills huge liquor business overnight ...

We've been researching the circumstances of a once highly successful liquor manufacturing business, with a huge client base - domestically as well as...

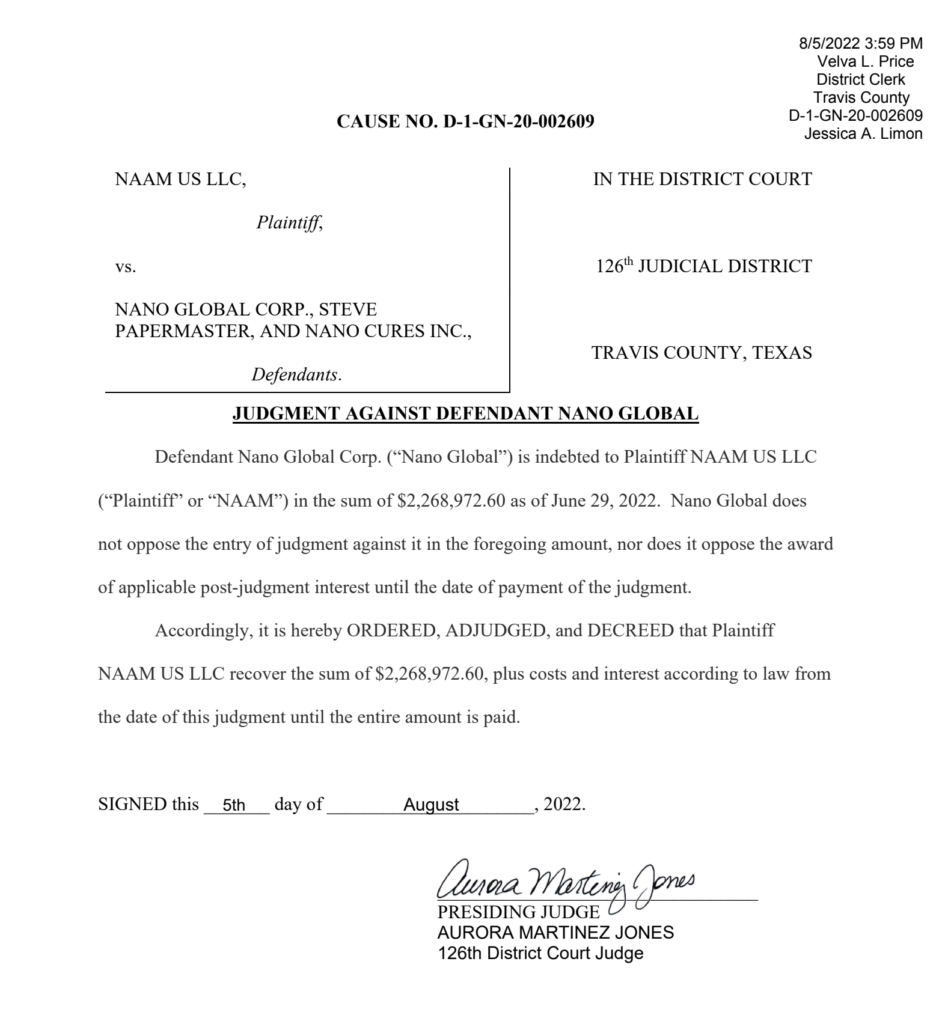

NAAM US LLC v Steve Papermaster, Nano Global Inc - judgment order

3 min read

Direct Fibreglass Pools: Customer Reviews, Complaints and Red Flags

About Direct Fibreglass Pools is the business name of Richard Andrew Mirosevich. Mirosevich is a frequent litigant. More information on...

1 min read

Instapools: Customer Reviews, Complaints and Red Flags

Public Reviews As at 10/2/2024. Source : https://www.facebook.com/groups/1407260559603442/search/?q=mirosevich Mabel R (Name...