1 min read

96 min read

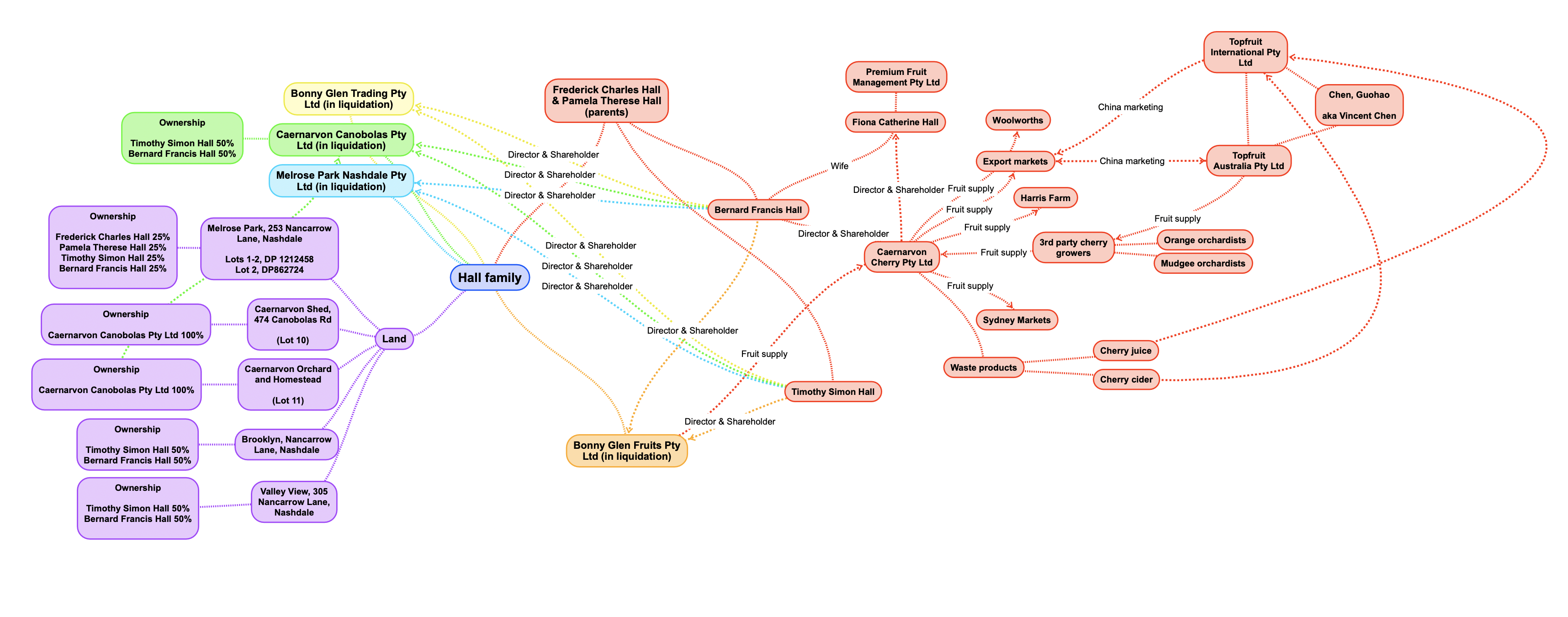

Caernarvon Canobolas Pty Ltd (in liquidation) - NSW Supreme Court Case 2018/340546

Current projects

Past projects

Blog

Case note

5R's

Defendant profile

Caernarvon Cherry

podcasts

Video

Defendant profiles

Orange

Corporate insolvency

Liquidators

Class Action

Projects

Caernarvon Cherry Co

Hall family

Liquidation

Profile

Bonny Glen (in liquidation)

class actions

AB Gartrell Philippines

Orange NSW

Fruit growers

Hall family Orange

Cash businesses

Fred Hall

Biteriot

Horticultural Produce Agreements

Bernard Hall

Fiona Hall

Fruit packers

Horticultural Code of Conduct

Caernarvon Canobolas Pty ltd in liquidation

Biteriot Operations

[2022] NSWSC 382

[2022] NSWSC 382

published 29 August 2022

Decision extracted and sourced from: https://www.caselaw.nsw.gov.au/decision/17ff234b71f1540bb837f52a#

Medium Neutral Citation:

In the matter of Caernarvon Canobolas Pty Ltd (In Liq) [2022] NSWSC 382

Hearing dates:20 – 23 July and 10 – 11 August 2021

Decision date:05 April 2022

Jurisdiction:Equity

Before:Ward CJ in EqDecision:

1. The appeal be allowed.

2. The liquidator’s determination to admit the proof of debt dated 15 November 2019 submitted by the second and third respondent be set aside and the proof of debt be rejected.

3. The second and third respondents pay the costs of:

(a) the applicant and the first respondent of and incidental to the amended interlocutory process in this proceeding; and

(b) the applicant and the first respondent (including liquidation costs, expenses and liquidators’ remuneration) of and incidental to the submission, consideration and determination by the liquidators of the proof of debt dated 15 November 2019 submitted by the second and third respondents.Catchwords:

CORPORATIONS – Winding up – Proceedings against company – Where debt disputed – whether parties reached agreement that costs of renovations would be recorded as a loan against the company

EVIDENCE – Documentary evidence – Business records – whether records were contemporaneous or issued retrospectively

ESTOPPEL – Promissory estoppel – Existing or expected legal relationship – whether the Company accepted or acquiesced to a benefit to the detriment of the second and third respondents

EQUITY – Equitable remedies – RestitutionLegislation Cited:

Corporations Act 2001 (Cth), ss 286, 477(2B), Schedule 2

Evidence Act 1995 (NSW), ss 48, 57(1), 58(1), 69

Supreme Court (Corporations) Rules 1999 (NSW), r 14.1(5)

Trustee Act 1925 (NSW), s 81Cases Cited:

Angas Law Services Pty Ltd (in liq) v Carabelas (2005) 226 CLR 507; [2005] HCA 23

Australia and New Zealand Banking Group Ltd v Westpac Banking Corporation (1988) 164 CLR 662; [1988] HCA 17

Australian Competition and Consumer Commission v Air New Zealand Ltd (No 1) (2012) 207 FCR 448; [2012] FCA 1355

Brick & Pipe Industries Ltd v Occidental Life Nominees Pty Ltd (1992) 6 ACSR 464; [1992] 2 VR 279

Briginshaw v Briginshaw (1938) 60 CLR 336; [1938] HCA 34

Broadway Plaza Investments Pty Ltd v Broadway Plaza Pty Ltd [2020] NSWSC 1778

Brodyn Pty Ltd v Dasein Constructions Pty Ltd [2004] NSWSC 1230

Capital Securities XV Pty Ltd (formerly known as Prime Capital Securities Pty Ltd) v Calleja [2018] NSWCA 26

Capocchiano v Young [2013] NSWSC 879

Commercial Union Assurance Company of Australia Ltd v Ferrcom Pty Ltd (1991) 22 NSWLR 389

Commonwealth v Verwayen (1990) 170 CLR 394; [1990] HCA 39

Damberg v Damberg (2001) 52 NSWLR 492; [2001] NSWCA 87

David Securities Pty Ltd v Commonwealth Bank of Australia (1992) 175 CLR 353; [1992] HCA 48

DHJPM Pty Ltd v Blackthorn Resources Ltd (2011) 83 NSWLR 728; [2011] NSWCA 348

Doueihi v Construction Technologies Australia Pty Ltd (2016) 92 NSWLR 247; [2016] NSWCA 105

Effem Foods Pty Ltd v Lake Cumberline Pty Ltd (1999) 161 ALR 599; [1999] HCA 15

El-Saafin v Franek (No 3) (2019) 143 ACSR 452; [2019] VSC 155

Falcke v Scottish Imperial Insurance Co (1886) 34 Ch D 234

Farah Constructions Pty Ltd v Say-Dee Pty Ltd (2007) 230 CLR 89; [2007] HCA 22

Federal Commissioner of Taxation v Cassaniti (2018) 266 FCR 385; [2018] FCAFC 212

Fitzgerald v F J Leonhardt Pty Ltd (1997) 189 CLR 215; [1997] HCA 17

Gregg v The Queen (2020) 355 FLR 348; [2020] NSWCCA 245

Grundt v Great Boulder Pty Gold Mines Ltd (1937) 59 CLR 641; [1937] HCA 58

Herdegen v Commissioner of Taxation (Cth) (1988) 84 ALR 271; [1988] FCA 699

Hill v Esplanade Wollongong Pty Limited (subject to a deed of company arrangement) [2018] NSWSC 478

Hutchinson v Sydney (1854) 10 Ex 438

In re Bailey, Hay & Co Ltd [1971] 1 WLR 1357

In re Express Engineering Works Ltd [1920] 1 Ch 466

In re Oxted Motor Co Ltd [1921] 3 KB 32

In the matter of Azmac Pty Ltd (In Liq) (2020) 146 ACSR 113; [2020] NSWSC 204

In the matter of Hillsea Pty Limited [2019] NSWSC 1152

Johnston v McGrath (2008) 67 ACSR 169; [2008] NSWSC 639

Jorden v Money (1854) 5 HL 185

Legione v Hateley (1983) 152 CLR 406; [1983] HCA 11

Lumbers v W Cook Builders Pty Ltd (in liq) (2008) 232 CLR 635; [2008] HCA 27

MYT Engineering Pty Ltd v Mulcon Pty Ltd (1999) 195 CLR 636; [1999] HCA 24

Parker & Cooper Ltd v Reading [1926] Ch 975

Pavey & Mathews Pty Ltd v Paul (1987) 162 CLR 221; [1987] HCA 5

Re ACN 096 281 542 Ltd (in liq) [2018] VSC 425

Re Duomatic Ltd [1969] 2 Ch 365

Re St Gregory’s Armenian School Inc (2015) 109 ACSR 27; [2015] NSWSC 1465

Rickard Constructions Pty Ltd v Rickard Hails Moretti Pty Ltd [2004] NSWSC 984

Rosseau Pty Ltd (in liq) v Jay-O-Bees Pty Ltd (in liq) (2004) 50 ACSR 565; [2004] NSWSC 818

Ryan v Dries [2002] NSWCA 3; (2002) 10 BPR 19,497

Spencer v The Commonwealth (1907) 5 CLR 418; (1907) 14 ALR 253

Sutherland (in his capacity as liquidator of Sydney Appliances Pty Ltd (in liq)) v Robert Bosch (Australia) Pty Ltd (2000) 33 ACSR 680; [2000] NSWSC 32

Tanning Research Laboratories Inc v O’Brien (1990) 169 CLR 332; [1990] HCA 8

Waltons Stores (Interstate) Ltd v Maher (1988) 164 CLR 387; [1988] HCA 7

Watson v Foxman (1995) 49 NSWLR 315

Westpac Banking Corp v Totterdell (1998) 20 WAR 150; (1998) 29 ACSR 448

Winterton Constructions Pty Ltd v Hambros Australia Ltd (1991) 101 ALR 363Texts Cited:

P L Davies, Gower and Davies’ Principles of Modern Company Law (7th ed, Sweet & Maxwell, 2003)Category:Principal judgmentParties:Timothy Hall (Plaintiff)

Bonny Glen Fruits Pty Ltd (First Defendant)

Bernard Hall (Second Defendant)

Bonny Glen Trading Pty Ltd (Third Defendant)

Caernarvon Canobolas Pty Ltd (Fourth Defendant)

Melrose Park Nashdale Pty Ltd (Fifth Defendant)

Frederick Charles Hall (Sixth Defendant)

Pamela Therese Hall (Seventh Defendant)Representation:Counsel:

D Smallbone with A Smyth (Applicant)

A Spencer (2nd and 3rd Respondents)

Solicitors:

MC Lawyers & Advisers (Applicant)

Matthews Folbigg Pty Ltd (2nd and 3rd Respondents)

File Number(s):2018/340546

Publication restriction:Nil

JUDGMENT

- HER HONOUR: By amended interlocutory process filed on 5 November 2020, the applicant (Timothy Hall) appeals from the decision of the liquidators of the first respondent (Caernarvon Canobolas Pty Ltd ACN 089 276 808 (In Liquidation), to which I will refer as the Company) to admit a proof of debt dated 15 November 2019 that was lodged by the second and third respondents (Bernard and Fiona Hall) on 26 November 2019. In that proof of debt, Bernard and Fiona claim the sum of $800,000 as due under an oral loan agreement alleged with the Company. Timothy seeks to set aside the determination of the liquidators (who have been joined together as the fourth respondent in the proceeding). The moneys claimed in the proof of debt relate to expenditure made by Bernard and Fiona on the Homestead occupied by them (rent free) on land then owned by the Company in Canobolas, New South Wales (the Canobolas Property). Fiona and a company associated with Bernard and Fiona have since acquired the Canobolas Property.

- The appeal is a hearing de novo, brought pursuant to s 90-15 of Schedule 2 to the Corporations Act 2001 (Cth) (Corporations Act), the Insolvency Practice Schedule (Corporations), (see Hill v Esplanade Wollongong Pty Limited (subject to a deed of company arrangement) [2018] NSWSC 478 at [21] per Gleeson JA). There is no dispute between the parties as to the principles that apply to such an appeal (see Re ACN 096 281 542 Ltd (in liq) [2018] VSC 425 at [6] per Randall AsJ; El-Saafin v Franek (No 3) (2019) 143 ACSR 452; [2019] VSC 155 at [63] per Lyons J; In the matter of Azmac Pty Ltd (In Liq) (2020) 146 ACSR 11; [2020] NSWSC 204 at [41] per Rees J); although there was some dispute in submissions as to the question of onus.

- Bernard and Fiona point to authorities to the effect that the party appealing against the liquidator’s decision (here, Timothy) bears the onus of showing that the decision was wrong; and that, if the onus is not discharged, the liquidator’s decision stands (see Westpac Banking Corp v Totterdell (1998) 20 WAR 150; (1998) 29 ACSR 448 at 451; Brodyn Pty Ltd v Dasein Constructions Pty Ltd [2004] NSWSC 1230 at [32]-[33] per Young CJ in Eq; Capocchiano v Young [2013] NSWSC 879 at [46] per Kunc J; Re St Gregory’s Armenian School Inc (2015) 109 ACSR 27; [2015] NSWSC 1465 (Re St Gregory’s Armenian School)). Timothy, on the other hand, says that the liquidators did not turn their minds to the question of contract, and did not accept that there was a restitutionary claim (T 367.24-48). Moreover, Timothy says that there is a lack of contemporaneous record or other satisfactory corroboration of the existence of a contract, which he argues places the case “squarely in Watson v Foxman territory” (referring to the oft-cited decision of Watson v Foxman (1995) 49 NSWLR 315). Timothy submits that the effect of this is that Bernard and Fiona bear the onus of establishing the proposition for which they contend in their points of claim (T 25.43).

- The relevant issue to be determined on an appeal such as this is as to whether the liability claimed or referred to in the proof of debt is a true liability of the company enforceable against it (see Tanning Research Laboratories Inc v O’Brien (1990) 169 CLR 332; [1990] HCA 8 at 339-340 per Brennan and Dawson JJ). On such an appeal, the party claiming to be a creditor of the company (here, Bernard and Fiona) is not strictly confined to the allegation(s) by which it originally sought to advance the proof of debt; it being said that “[a]s long as the claim remains the original claim, some change in the explanation of the way in which it is said to be a true liability of the company enforceable against it is permitted” (Johnston v McGrath (2008) 67 ACSR 169; [2008] NSWSC 639 at [26] per Barrett J; and see Rosseau Pty Ltd (in liq) v Jay-O-Bees Pty Ltd (in liq) (2004) 50 ACSR 565; [2004] NSWSC 818; Re St Gregory’s Armenian School).

Background and chronology of events

The family business

- For convenience, I will generally refer to the Hall family members by their first names. The applicant (Timothy) and the second respondent (Bernard) are brothers. Their parents (Fred and Pamela) established a fruit growing business near Orange (operating through a number of companies and from a number of properties located in two adjoining districts, Canobolas and Nashdale, on either side of the Towac Valley). The first such property was known as the Bonny Glen Property. The fruits that were grown, packed and sold were principally apples and cherries (see [5] of Timothy’s first affidavit sworn 16 April 2021).

- Timothy started working in the family orchardist business full time in 1978. Bernard, who is around eleven years younger, commenced work in the family business either in 1989 (on Timothy’s version of events – see Timothy’s 16 April 2021 affidavit at [6]) or a few years earlier when aged 16 (on Bernard’s version of events). Nothing turns on the difference in the respective versions of events in this regard.

- In about 2004, Bernard and his wife, Fiona, incorporated their own company (Caernarvon Cherry Pty Ltd) through which they traded separately from the family business. (It appears that the operation of this business was a cause of some disagreement between the brothers – see, for example, Timothy’s first affidavit at [30]).

- Prior to 2007, the main trading company for the family business was Bonny Glen Pty Ltd; after 2007 (when Fred and Pamela retired from the business) a different company, Bonny Glen Fruits Pty Ltd, was the main trading company (see Timothy’s first affidavit at [12]). The Company owned the land and improvements at the Canobolas Property but did not trade.

- From 2007 (until 27 November 2018), the family business (known as Bonny Glen Fruits) was largely operated by Timothy and Bernard, who also controlled the various companies associated with the business, although their parents are said to have maintained some ongoing (informal) involvement in the business. From 2011, Timothy and Bernard each owned 50% of the shares in the Company.

The Nashdale (or Melrose) Property

- In 1992, the Nashdale Property (referred to in some of the evidence as Melrose) was acquired jointly by Fred, Pamela, Bernard and Timothy. This property was adjacent to a property known as Brooklyn (that property itself being adjacent to the originally acquired Bonny Glen Property).

- In around 1997, the Nashdale Property was subdivided to create a parcel of six acres which was transferred (at no cost) to Timothy and his then wife, Jennifer, who then built a house on the land. (It is noted by Bernard and Fiona that Bernard received nothing for his interest in that portion of land.) The parcel of land transferred to Timothy and Jennifer (known as Melrose Park) was subsequently sold by Timothy and Jennifer in 2001, following the breakdown of their marriage. Following his separation from Jennifer (apart from a short time at the Bonny Glen Property), Timothy resided (and from 2004 did so with his wife, Robyn) in Melrose Cottage, which was located on the main Nashdale Property, until about 2019.

- In around 2007, Timothy and Bernard bought Brooklyn from their parents and in 2013 they jointly acquired another property in Nashdale (see Bernard’s first affidavit sworn 19 April 2021 at [44]-[45]).

- Timothy has, as I understand it, largely controlled or managed the Nashdale side of the family business operations; Bernard and Fiona, the Canobolas side of the operations.

Canobolas Property

- The Canobolas Property was acquired by the Company in September 1999 for $630,000. The Company was formed for the purpose of making that acquisition. On its incorporation, each of Fred, Pamela, Bernard and Timothy was a director of the Company and each held one of the four issued shares. In 2010, Fred and Pamela retired as directors and in 2011 Bernard and Timothy each acquired one of their parents’ shares. Accordingly, by the time of the events in question, each of Bernard and Timothy was a 50% shareholder of the Company. As adverted to above, at all relevant times the operations of the family business that were conducted on the Canobolas Property were managed by Bernard and Fiona.

- From late 1999, Bernard and Fiona have resided in a house known as “the Homestead” located on the larger of the two lots (Lots 10 and 11) comprising the Canobolas Property. On the other (smaller) of the two lots is a packing shed housing the relevant equipment and other infrastructure for the processing and packing of the fruit grown in the family business (and also, as I understand it, in Bernard and Fiona’s separate cherry growing business); as well as an office.

Corporate compliance

- For the most part, compliance with the corporate and regulatory requirements of the companies through which the family business was conducted was carried out with the assistance of an accountant (Mr Desmond Lee), who travelled to Orange from Sydney once a year with relevant company documents to be executed following the holding of formal meetings with the directors and shareholders (such meetings being held, first, at Fred and Pamela’s house (on the Bonny Glen Property) and then at the Canobolas Property).

- Bernard and Fiona describe these company documents as “vanilla” corporate governance documents (T 8.4). They point out that the minutes of company meetings were prepared in advance by Mr Lee, who brought them with him to the annual meetings; and they contend that therefore that the minutes could not (unless, I would add, later amended) reflect any matters discussed at the relevant meetings. They also point out (correctly) that the company documents are replete with errors – from time to time identifying the directors wrongly; being signed by people who were not directors; and recording persons who owned no shares as attending in the capacity of shareholders (see T 8). Thus, it is said that the brothers cannot carefully have reviewed them. It is submitted (and there is some force in this submission) that the holding of meetings and recording of minutes for the various companies associated with the business were matters treated by family members as a formality.

- Bernard and Fiona describe Mr Lee as more than just an accountant. They say that he was a trusted adviser, who advised the family members as to the structures to be put in place for or in relation to the business and as to their personal and corporate tax affairs. That may well be the case but, as I explain in due course, that does not to my mind cloak Mr Lee with authority to bind any of the family members or the Company in their dealings with each other.

- Timothy (see from [35] of his 16 April 2021 affidavit) describes the typical yearly meetings with Mr Lee, including that there would be separate meetings with the shareholders and directors of the relevant companies from those in relation to personal tax matters or meetings relating to “Caernarvon Cherry related matters”. Mr Lee’s evidence as to those matters is consistent with that of Timothy on this issue.

Deterioration in the relationship between the brothers

- At some point there was evidently a deterioration in the relationship between the two brothers (although there is some contention as to when this commenced). Timothy places this as occurring from about the late 2000s, from which time he says that he and Bernard were estranged and only saw each other a few times a year (see at [33] of his affidavit dated 16 April 2021). As adverted to above, it appears that this (if not wholly attributable to, then at least) may have been exacerbated by the establishment by Bernard and Fiona in about 2004 of their own separate cherry growing business from the Canobolas Property. Fiona herself says that the relationship between Timothy and Bernard became “toxic” but places this as occurring in 2016 after a heated argument between the brothers in that year (see Fiona’s first affidavit sworn 19 April 2021 at [30]; and see notes dated 8 February 2017, apparently made by Timothy having regard to their content, in which there is reference to an issue as to the poor delivery of the spray programme). Consistent with this note, Bernard places the deterioration in the relationship as occurring by 2017.

Desire of Bernard and Fiona to renovate the Homestead

- The Homestead was originally built in about 1910. By 2012, Bernard and Fiona, who then had three young children, wished to renovate the house (which they say was in need of significant repair). As noted, by that time Bernard and Timothy were the only directors and shareholders of the Company, which owned the Canobolas Property.

14 September 2012 meeting

- Featuring prominently in the evidence and submissions were two meetings, the first of which is said to have taken place on 14 September 2012 at Fred and Pamela’s house during a lunch (or perhaps morning tea) attended by Timothy, Bernard and Fiona, Fred and Pamela (see Bernard’s first affidavit at [144]; Fiona’s first affidavit at [79]). It is not suggested that Mr Lee was in attendance at that meeting. Indeed, Mr Lee’s evidence is that he was not present in Orange on 14 September 2012 (being in attendance at an all day meeting with another client in Sydney) and he did not know if there had been a meeting on that day (see at [32] of Mr Lee’s first affidavit sworn 19 April 2021).

- Bernard has deposed (at [144]) that, at this lunch, there was a discussion about the family business, during which there was the following conversation:

[Bernard] said: Fiona and I want to renovate the Homestead to fix some issues and make the house bigger for our kids. We have the money, and can use our own, but we are worried about what will happen if the Company ever sells or transfers the house. We want to make sure that we can get that money back if the Homestead is ever sold or transferred.

Tim said: Before you think about renovating, why don’t you look at subdividing the lot like I did at Melrose. If that doesn’t work then you can do the renovations.

[Bernard] said: Okay, Fiona and I will look into that and let you know how it goes.

- Bernard has deposed that, following that conversation, Fiona and he attended a consultation with Mr Peter Basha, the town planner, about a possible subdivision; and that Mr Basha subsequently advised them that the Council would not permit the subdivision because the packing shed (on the smaller of the two lots) was on an industrial lot and that they could not combine that back with the main lot (see Bernard’s affidavit at [146]-[147]).

- Fiona’s account of this discussion (see from [79] of her first affidavit) is that the conversation occurred at a morning tea with Bernard, Timothy, Robyn, Fred and Pamela at the Bonny Glen Property. Fiona deposes that she took notes of the discussion because Mr Lee had earlier said to Timothy and Bernard that they needed to begin having meetings and recording the discussions; and that, as Mr Lee did not attend this meeting she took a record for Mr Lee (see at [81]). Fiona also deposes that at the beginning of the discussion she asked everyone’s permission to take notes and that Pamela approved this (see at [84]).

- Fiona has deposed that Bernard raised that they wanted to undertake renovations of the Homestead in words to the following effect:

Bernard said: We need to do some work to the Homestead because the old electricity is dangerous and we now have 2 young children and a Toddler. We want to renovate but it’s going to cost a lot because it’s an old house and like opening a can of worms, so our money needs to be recognised. We need bathrooms, a new laundry, electricity, new bedrooms, proper heating and such.

Tim said: Why don’t you go and look at other ways first like look at buying Armstrong’s [next door neighbour’s at Melrose] place or buying another house somewhere.

Pam said: Or why don’t you see if you can move the title and get 6 acres like Tim did? You’ve got these little kids and need something sorted as we just had a cold winter and the place is freezing. Something needs to be sorted.

Bernard said: Okay, we’ll look at other options.

- Fiona also deposes to a consultation with Mr Basha about the proposed subdivision and to Bernard’s account of the Council’s position shortly after that consultation (see [88]-[90] of Fiona’s first affidavit), which is consistent with Bernard’s recollection.

- Bernard and Fiona refer to the above evidence and say that they told those present at the meeting that they were prepared to use their own funds to pay for the renovations at the Homestead but wanted to be able to recover those funds if the Company or the property was ever sold. They also say that Timothy said that, if the Canobolas Property could be subdivided and a small block transferred to Bernard and Fiona, he would consent to the subdivision and Bernard and Fiona could build a new home on the subdivided block. (The above summary by Bernard and Fiona of the conversation does not wholly accord with their affidavit evidence; in which they attribute to Timothy suggestions about other options such as buying another property or subdivision but not consent in terms to the subdivision option.)

- Fiona’s handwritten notes of the meeting of 14 September 2012 (which she says, but Timothy and Mr Lee seem to dispute, she took at the meeting) record the presence of Timothy and Robyn, Bernard and Fiona and Pamela and Fred; that the meeting went from 9am to 10.30am; and, among other things, that:

- House @ Caernarvon

B&F expressed wanting to renovate house but for $ sunk into place to be recognised.

Tim suggest to look @ other options.

- At the conclusion of the notes there appears an entry in a different coloured pen. This page of the notebook was followed by a printed document headed “A snapshot as of 13th September 2012”, which appears to correspond to the entry in the handwritten notes “Fiona gave snapshot of season to date (enclosed)”. This suggests that at least part of the notes (such as the pasting of the printed note into the book) was compiled after the meeting. Immediately following the second page of the pasted typed sheet are handwritten notes headed “Monday 1st October 2012” starting in a blue pen and then changing to a black pen. There was a suggestion that one of the entries “follow Des up 400k” was in Bernard’s handwriting (T 110.40). The following page (whimsically headed Maggie’s minutes) was obviously a child’s scribblings.

- Timothy (see at [56] of his first affidavit) deposes that he does not recall the entirety of the conversations concerning improvements to the Homestead and cannot be sure when each conversation took place, or in which years, or the order of the conversations or exact words used. Timothy did recall one of those conversations (at [59] of his first affidavit) (which he says was in the dining room at his parents’ house during an annual visit of Mr Lee) in which he says that Bernard said that the house was very cold in winter and they needed to update the heating (which he says he queried but then, after Bernard said they needed heating, to which he said “OK”); and that during one of the annual meetings Bernard said words to the effect that the house needed to have new heaters put in and that they wanted to do a new bathroom (see at [63]).

- Bernard and Fiona submit (at [33] of their written submissions) that the parties’ accounts of what happened at this meeting (and the subsequent 16 May 2013 meeting) should be read in light of the fact that what occurred at the meeting was specifically pleaded in their Points of Claim and put in issue by Timothy’s Points of Defence. Essentially, Bernard and Fiona submit that Timothy’s denial that the two meetings occurred as they described is not supported by his own evidence of what occurred at those meetings. This submission appears to be directed towards the argument that Timothy has failed to discharge the onus of proof to support a finding that the liquidator’s decision was wrong.

- To this end, Bernard and Fiona emphasise that, in his first affidavit, Timothy gave no specific evidence about the meeting of 14 September 2012 and conceded that he did not “recall the entirety of conversations that took place concerning improvements to the house at [the Canobolas Property]”. (As noted, there is no suggestion that Mr Lee was at the meeting of 14 September 2012.)

- In his second affidavit sworn 17 May 2021, Timothy responded to various aspects of the affidavit evidence of Bernard and Fiona with which he disagreed. It is noted that Timothy did not traverse [144] of Bernard’s first affidavit (set out above) but that he did reject those parts of the conversation recorded in Fiona’s account (see above) that referred to “electricity, Melrose or Armstrong’s property” and instead deposed to having suggested a different property. Bernard and Fiona emphasise that Timothy did not specifically contradict that part of the conversation in which Bernard expressed the aim that their expenditure of funds be recognised. (Pausing here, what is not here made clear is precisely how it was contemplated by Bernard that their funds would be recognised; nor is it suggested that Timothy agreed to any such arrangement at this meeting. I also interpose to note that Bernard and Fiona do not suggest that any agreement was reached at this meeting; rather, they rely on this as context or background.)

Prospect of Subdivision

- As noted above, Bernard and Fiona depose that, following the 14 September 2012 meeting, they explored the prospect of a subdivision of the Canobolas Property (by speaking with Mr Basha, the town planner) and that they were advised that it would not be possible. They say that Timothy was aware of that (a reference seemingly to the account given by Bernard of the conversation on 16 May 2013 – see below).

16 May 2013 meeting

- The second of the two meetings on which Bernard and Fiona here place emphasis (and at which they say a binding agreement was reached) was a meeting that took place on or about 16 May 2013 during one of Mr Lee’s annual visits to Orange.

- Mr Lee deposes that the meeting took place at Fred and Pamela’s residence; and he describes in his affidavit a series of meetings on this day (see from [35]).

- First, a meeting of the Bonny Glen Fruits Pty Limited Group (attended by Timothy, Bernard and Fiona) to review the financial accounts and taxation for the financial year 2012 and interim accounts for 2013 and for the signing of the 2012 accounts and financial returns, at which meeting he deposes that Fiona said words to the effect that they currently needed better heating at that Homestead and Timothy said he had no problem with them improving the heating. Mr Lee did not recall anyone taking notes on that occasion.

- Second, a meeting with Timothy alone in which Mr Lee presented to him the company’s financial statements and taxation returns and personal returns for the financial year ending 30 June 2012, following which meeting he says Timothy immediately left the house, saying that he was taking the documents home to Robyn so that they could sign them (and Timothy returning later in the afternoon with signed documents).

- Third, while Timothy was out of the house, a meeting only with Bernard and Fiona to review their entities’ financial statements taxation and personal returns for 30 June 2012.

- Fourth, a meeting with Pamela and Fred for them to review and sign their own company’s financial accounts and their personal tax returns.

- Mr Lee did not see any minutes book or hard-bound blue book (Exhibit 12) on that day (see at [44] of his affidavit of 19 April 2021). He deposes that he did not add any further resolutions to the formal draft minutes that he had prepared in advance for the Company meeting and that he was not asked to prepare any such notes or minutes. Mr Lee did, however, earlier depose that at some meetings he saw Fiona take notes (see at [20]).

- Relevantly, at [64] of his affidavit of 19 April 2021, Mr Lee deposed that at none of the yearly meetings had he heard that Fiona or Bernard wanted to claim reimbursement from the Company for the costs of the renovations for the Homestead. (That is consistent with their account being that they wanted some unspecified recognition in the future of their expenditure.)

- Bernard’s evidence of the meeting was that it was at a lunch at the Caernarvon Cottage with Fiona, his parents, Mr Lee and Timothy. Bernard deposes that the conversation was to the following effect:

[Bernard] said: We spoke to a town planner and they won’t let us subdivide the lot. We still want to update the Homestead and extend it, so we want to go ahead with the renovations. How do we go about that?

They said: Where will you get the money from?

[Bernard] said: We can pay for the renovations ourselves or through Caernarvon Cherry, but we want all the money we put into the Homestead to be recognised if the place is ever sold or transferred to someone else.

Des said: You should also get a valuation before you do the renovations, and then another valuation after so you can see how much the Homestead is improved. It could be important if you need to pay some tax on it in the future.

[Bernard] said: Okay, we can do that. But more importantly we want to get our money back that we put in, so we want the money we spend on the renovations to be accounted for by the Company somehow.

Des said: Okay. Keep your receipts so that we can see how much you spend on the renovations and we can put that in the records of the Company as a debt owed to you and Fiona. Then the Company can easily pay you back if the Homestead ever sells. We can also make sure that you get paid interest, for example at an interest rate equivalent to the change in the Consumer Price Index until you are repaid.

[Bernard] said: That sounds like it does everything we want, let’s do that.

Des said: Does everyone agree to doing it that way?

Tim said: Yeah, I’m okay with that.

- Bernard has deposed that he saw Fiona writing in the minute book during that meeting and identifies in his affidavit the notes of that meeting.

- Fiona’s evidence is that this meeting was at “another lunch” with Bernard, Timothy, Fred and Pamela, at Pamela and Fred’s house at Bonny Glen, for the purpose of going over the accounts and financials with Mr Lee who had travelled from Sydney. Fiona says that the meeting was while sitting around the kitchen table and that there was a discussion in words to the following effect:

Bernard said: We’ve been told we can’t do a subdivision so we’re back to the drawing board and want to renovate 474 Canobolas.

Armstrong’s place want too much money and we want to stay on the property and don’t want to be living at Melrose and working at Caernarvon. Either way, it isn’t an option to build another house on Caernarvon because we’d have the same issues with wanting the money to be recognised because it would be Company land. So, we think we may as well renovate the Homestead.

Tim said: Okay.

Bernard said: We aren’t asking for money, just asking if we can spend own money on the place because we would be doing large scale renovations. How can we have our money recognised?

Des said: Keep all your receipts so that we can see how much you spend on the renovations and I’ll put that on the books of the Company. Each year we can add the CPI to the amount you’ve spent and it’ll be on the books as a loan. But if you do overcapitalise [sic]

Bernard said: Okay let’s do that. That’s fine, we will be responsible if we overcapitalise.

- Fiona goes on to depose that she is unable to recall whether the subject of valuation was raised at the 16 May 2013 meeting or whether it was raised in a later discussion but that, at some point after the 16 May 2013 meeting, she was present at a conversation between Timothy and Bernard in words to the following effect:

Des said: Get a valuation before you do the renovations, and then another valuation after that so that you don’t overcapitalise.

We said: Okay, if we do then that’s our money and we will be responsible for that.

- Fiona says that Timothy agreed with that proposition (at [94] of her first affidavit sworn 19 April 2021).

- Bernard and Fiona say that an agreement was reached at this meeting that they (Bernard and Fiona) would fund the renovations to the Homestead and that, if the property was ever sold, the Company would repay those amounts together with interest at a rate equivalent to the CPI. They say that it was also agreed that the amounts so expended would be recorded in the accounts of the Company as a debt owed to Bernard and Fiona. (Both Timothy and Mr Lee dispute this. For Timothy, it is said that this amounts in effect to arguing that the Company would give Bernard and Fiona a “blank cheque” to spend whatever they liked on the property and that this is implausible – see T 360.31. It would certainly be inconsistent with the attitude that Timothy appears to have displayed throughout the proceeding to the issue of expenditure by his brother.)

- As adverted to above, there were in evidence some handwritten notes made by Fiona (contained in the blue book – Exhibit 12) headed “Meeting Thurs 16th May 2013”, recording as present Timothy, Bernard, Fred, Pamela and Fiona but also referring to a presentation by Mr Lee. The notes (on which there is some scribble in a different colour pen) include that:

Bernard spoke of Renovations required at Caernarvon house. Des advised to keep records of amounts spent so that amounts will be recorded & owed to B & F & increased in CPI’s.

- Bernard and Fiona emphasise that both their affidavit evidence and the notes record a conversation in which there was a discussion about the renovations, the money to be spent, and the amounts being recorded and owed to Bernard and Fiona. Bernard and Fiona note that, in response to that affidavit evidence, Timothy did not traverse the relevant paragraphs of Bernard’s affidavit (at [149]-[151] of his second affidavit sworn 17 May 2021) and, while specifically dealing with two other aspects of what was said, did not contradict Fiona’s account of what was said in relation to the recognition of their expenditure. Similarly, it is said that, while Timothy dealt specifically with inaccuracies in Fiona’s notes, he did not suggest they were inaccurate insofar as they recorded conversations at this or the earlier meeting.

- It is noted by Bernard and Fiona that, in his first affidavit, Mr Lee gave a lengthy account of what took place when he visited Orange on 16 May 2013 and the order in which he conducted the meetings on that day (as summarised above) but deposed to only one conversation that occurred on that day; whereas he gave a detailed account of a conversation on 26 March 2014 concerning proposed renovations to the house at Canobolas and the way in which Bernard and Fiona might be reimbursed for moneys expended (see below) (at [51] of Mr Lee’s first affidavit sworn 19 April 2021).

- In Mr Lee’s second affidavit sworn 17 May 2021, his response to [150] of Bernard’s affidavit is that he did not say the words attributed to him by Bernard nor did he hear Timothy say that “Yeah, I’m okay with that” (and Mr Lee affirms that his memory of that conversation is as set out at [51]-[53] of his 19 April 2021 affidavit). As to [92] of Fiona’s first affidavit, Mr Lee deposes that he does not recall this conversation occurring during the lunch at Fred and Pamela’s house on 16 May 2013 “or at any other occasion”. Bernard and Fiona say that there is an obvious similarity between that conversation and the one recounted at [51] of Mr Lee’s first affidavit – both accounts refer to Mr Lee’s suggestion that the renovation costs be recorded as a loan in the company records and that CPI adjustments be made; however, it is noted that only Mr Lee deposes that he said items were to be approved by Timothy and Bernard.

- Further, Mr Lee cavils with the statement by Fiona at [93] of her first affidavit that an agreement had been reached. Mr Lee asserts that he did not hear words of agreement or that there was an agreement; rather, he deposes that there were options discussed (but his recollection is that this was at the 2014 meeting rather than at the 2013 meeting).

- In oral submissions, it is said for Bernard and Fiona that, at the 16 May 2013 meeting, the Company (by representations and statements by Timothy and Mr Lee) “bound itself to treat amounts which Bernard and Fiona were to spend on renovations for the Company’s house as loans in the books of the company to carry interest” (see T 6). Insofar as Bernard and Fiona rely on statements by Mr Lee, there is nothing on the evidence to support a conclusion that Mr Lee had any authority to bind the Company; at most, his statements would be relevant to the extent (which is debatable) that it could be said that Timothy (by silence or otherwise) had adopted them.

Credit issues specific to the two meetings

- As to the two relevant meetings (the 14 September 2012 meeting and the 16 May 2013 meeting), on the question of credit Bernard and Fiona point to the following matters.

- First, that in their affidavit evidence both Mr Lee and Timothy sought to convey the impression that the yearly meetings were conducted with a formality that elevated the significance of the absence of entries in the minutes and financial records recording what took place at the meeting of May 2013; yet Mr Lee conceded that there was no separate meeting of the shareholders of the Company and that neither Timothy nor Bernard had ever raised for attention the fact that some of the documents which they had executed indicated the wrong directors and the wrong shareholders nor had they ever asked him to add further resolutions to the Company’s draft minutes.

- Second, that Timothy was quite frank about his lack of specific recollection in relation to the meetings; nevertheless, it is said that he sought to minimise the length of the meetings and that he denied some very obvious propositions about them (including that the bulk of the time spent in the meetings concerned the operations of Bonny Glen Fruits and that Fiona attended that meeting). It is noted that Timothy insisted that he reviewed the minutes that he signed to ensure the details were correct, when it is said that they were replete with errors that would have been obvious on any such review (see, for example, minutes of the meeting of directors of the Company on 10 December 2012, which record the four family member as directors when Pamela and Fred had ceased by then to be directors; and of the shareholders meeting of 31 December 2012 which display a similar problem).

- Third, that Mr Lee gave generalised evidence about how the meetings were conducted (which Bernard and Fiona say no doubt reflected the many similar meetings that he had conducted with the family). It is submitted that it should be inferred that the meeting of 16 May 2013 followed the pattern which Mr Lee described in general terms in cross examination. However, Bernard and Fiona say that when it came to specific matters Mr Lee’s recollection was less impressive, noting that Mr Lee recalled only one short conversation about renovations at the meeting of 16 May 2013 with the aid of his affidavit. It is submitted that that recollection is to be considered in the light of Mr Lee’s complete lack of recollection when cross examined in relation to the conversations regarding the renovations that he had detailed at [51] of his first affidavit and the recollections set out at [6], [7], [8] and [12] of his second affidavit sworn 17 May 2021. Indeed, it is noted that Mr Lee could not remember what he had said of those matters in his affidavit sworn only three months before the hearing.

- Fourth, that in cross examination Bernard confirmed the existence of a verbal agreement whereby the company would repay the amounts expended for renovations or improvements on the property; readily made concessions; and confirmed that his wife took notes. Bernard and Fiona say that the accounts of the two meetings given by Bernard and Fiona are supported by contemporaneous notes made by Fiona. Insofar as it was put to Fiona that the relevant note was made after the event in an attempt to reconstruct, it is noted that Fiona rejected that suggestion. Bernard and Fiona say that the facts do not support that serious contention, referring to the objective evidence which showed that Fiona attempted over a number of years to ensure that notes were taken at meetings when the business of Bonny Glen Fruits was discussed (pointing to her blue book which contains notes of meetings on 14 September 2012; 1 October 2012; 16 May 2013; 26 March 2014; and 1 December 2015) and that there is contemporaneous evidence that Fiona asked Ms Leanne Pearce (who worked for Bonny Glen Fruits) to assist in keeping the minutes of the meetings (pointing to the copies of Leanne Pearce’s notes of meetings on 22 October 2015 and 5 June 2016).

- Pausing here, I do not accept that a conclusion that the notes were not all made during the actual meeting would necessarily connote some dishonest reconstruction of events. It is more plausible to my mind that the notes are an amalgam of jottings made at around the time of the meeting (potentially, some made before, some during and some after the meeting) rather than being wholly a verbatim note or summary of what was said that was taken during the meeting itself.

- Finally, in this context it is said (and I would accept) that the “patchwork” nature of these records speaks to their authenticity. It is said that the probabilities are that, if Fiona had intended to concoct a record reflecting consistent contemporaneous note taking and relevant notes, she would have collected all that material in the one place and using the one style (and most likely would have also protected this most valuable record from her young daughter’s scribblings).

- Therefore, I accept that the notes are genuine though not necessarily completely contemporaneous, and, moreover, they may record Fiona’s understanding as opposed to what was in fact said.

Arrangements for renovation works

- Bernard and Fiona say that, after the 16 May 2013 meeting, preparatory work for the renovations to the Homestead commenced (later in 2013). Bernard and Fiona arranged to have sketches made prior to drawing up plans (which they place as occurring about six months before they began the renovations – see [107] of Fiona’s first affidavit); paid to have plans drawn up (by McKinnon Designs – the plans being drawn from sketches taken on about 28 February 2014 – see [108] of Fiona’s first affidavit); sought out John Nunn Building Contractors Pty Ltd (John Nunn Building Contractors) and obtained a quote for the major part of the building works (which they place at approximately 26 March 2014 – see Fiona’s first affidavit at [114]); and they signed a contract for the major building works (on 22 May 2014), the contract noting drawings from McKinnon dated October 2013 (see contract provision regarding the drawings; and Fiona’s first affidavit at [115]).

- Bernard and Fiona also make reference to contemporaneous documents (see below) which it is said show that, shortly before signing the building contract, Fiona had communicated with Mr Michael Thornhill (a financial consultant who undertook some financial consulting work for Caernarvon Cherry at the time) as to clarification being sought that “personal funds you [Fiona] and Bernard/Caernarvon Cherry Pty Ltd [Bernard and Fiona’s company] have available will be used to pay for the house renovations, and there will be an adjustment done to square things up with Tim”. (To my mind it is significant that this leaves open how the adjustment was to be effected.)

Meeting on 26 March 2014

- Mr Lee has deposed (see from [47] of his first affidavit) to a meeting at the Bonny Glen Fruits Pty Ltd administration office in Orange on 26 March 2014 to discuss the financial statements for the Group and the signing of the Group financial statements and taxation returns for 30 June 2013. Mr Lee deposes to a conversation on that occasion in which he says Fiona raised the question as to “how would [they] be reimbursed” if they did some renovations to the house at Canobolas; that Timothy suggested looking at houses for sale nearby and subdivision as an alternative; and that:

Tim said: Perhaps one way if you were going to do any renovations to the house at Canobolas was to get a valuation of the house before and after the renovations. This way would work out what increase in the value was gained by such renovations rather than what you had spent.

[Des] said: Another way to record down what items you spent and from those items be approved by Tim and Bernard and recorded in the company financial records as a loan to you both (being the company financial records as a loan to you both (being Bernard and Fiona). Those costs could be adjusted by CPI and an adjustment made for each year of the increase in value as you could over capitalise the property and such costs not recovered in valuation method [sic]

- Pausing here, it seems to me more likely (having regard to the chronology of events) that this conversation occurred in the course of the May 2013 meeting rather than the March 2014 meeting because steps had already been taken by March 2014 at least for the obtaining of plans for the proposed renovation.

- Again, there are handwritten notes made by Fiona contained in the blue book of this meeting, recording the meeting with Mr Lee at Caernarvon Cottage and the presence of Timothy, Fiona and Bernard. Those notes do not record any of the above discussion to which Mr Lee deposed. There is then a lengthy gap in time before any further minutes or notes in the book – those recommencing with a typed set of minutes of a meeting on 1 December 2015 attended by Timothy, Bernard, Fiona and “LP” (which I infer to be Leanne Pearce).

Valuation by Andrew Saunders – April 2014

- Mr Saunders inspected and valued the Homestead (i.e., not the Caernarvon Property as a whole) on 29 April 2014 (the “before” valuation) at $770,000 (being land valued at $385,000 – for a site area of 2ha; and improvements at $385,000). Mr Saunders assessed the rental value unfurnished at $475 per week.

Communications with Mr Lee – April/May 2014

- I have referred above to the communications with Mr Thornhill.

- On 30 April 2014 (in response to a request made on 30 April 2014 by Mr Lee for Fiona to send an MYOB accounting file for Bernard and Fiona’s business entities), Fiona sent an email to Mr Lee stating “will do, we will have done by end of next week” but went on to ask Mr Lee to read a message received from Mr Thornhill and to confirm her explanation to Mr Thornhill (as to the funding of the house renovations) as well as to address the last paragraph of the message. The message from Mr Thornhill read:

Hi Fi

As discussed, I understand that personal funds you and Bern/Caernarvon Cherry Pty Ltd have available will be used to pay for the house renovations, and there will be an adjustment done to square things up with Tim based on the pre- and post- valuer of the house as it is owned by one of the Company’s that is 50% owned by Tim.

…

The other point that may be worth checking with Des is that the way you will be paying for the house renovations will be the most tax effective for the Company and yourselves individually. I suggest checking with Des to confirm that there are no other strategies he would suggest to assist with tax minimisation now and in the future.

- On 5 May 2014 (before the contract with John Nunn Building Contractors was signed), Mr Lee responded to Fiona’s 30 April 2014 email, saying:

It is my understanding at our meeting in Orange that Tim suggested pre and post valuation.

I suggested what ever [sic] you spent plus CPI would be adjusted and to resolve the issue I suggested the higher of the two.

The reason I explained you could over capitalise the property and such costs not recovered in the valuation.

With the current update to end of April figures you are sending I can work out the overall tax planning.

To assist please also provide estimate of renovations costs and timetable and what type of renovations.

- Bernard and Fiona say that it is common ground that the subject of the payment for the renovations was raised by Bernard and Fiona, and that Mr Lee had recorded resolution of the issue; and they point to these as matters going to the unlikelihood that they proceeded with the funding of the renovations without any agreement having been reached on that issue. The difficulty I have with that proposition is that there is not clear evidence of an agreement emerging from the above affidavit evidence, even on Bernard and Fiona’s account of the conversations. Rather, what is clearly apparent is that Bernard and Fiona wanted there to be recognition in some fashion of their expenditure (and most likely that this would be by some sort of adjustment or squaring up between the brothers in the future).

- For Timothy, it is said that for there to be acceptance of the position in relation to reimbursement of or recognition for the cost of the renovations, there has to have been knowledge of the costs of the renovations and the types of renovation (and it is noted that Mr Lee wanted an estimate of these to be provided).

- The above chronology of events shows that there were discussions about the proposed valuation of the property before and after the proposed works; and that it is made quite clear that no agreement was reached between the parties; rather, Mr Lee writes in the abovementioned email that his understanding was that Timothy and he both provided suggestions as to how the renovations could be reimbursed, and requested further details of the costs of the renovations and the type of renovations.

- On 13 May 2014, Fiona responded to Mr Lee, attaching the updated MYOB accounting file he had requested, in which email she said:

hi des

I have just emailed you the backup of MYOB for April 30. We have done as suggested and had the house (and house only) valued before any renovations commence. I will pass this on once received.

The renovations will commence next week however I don’t envisage a lot of money being spent before the end of the financial year. There have been costs to council, draftsman, engineering, design etc so far, however my prediction that another 70k would be spent before end of fy at the most.

The total renovation is going to be an estimated [sic] at $400-450k, will give you some more details when the fixed quote comes in from the builder tomorrow.

- Mr Lee has deposed (at [61] of his first affidavit) that he did not receive any further information regarding the renovations beyond the above communication; and that he did not think about forwarding a copy of this to Timothy because the email chain was part of the records between Caernarvon Cherry Pty Ltd and his firm; and Timothy had never been a director or shareholder of that company. There is no evidence that Timothy was made aware of this estimated cost.

Arrangements for building works

- The development application dated 15 April 2014 described the development as extensions and alterations to the cottage at an estimated cost of $350,000. The development application recorded the owner’s consent (of Bonny Glen Fruits) bearing the signatures of both Fiona and Bernard – Fiona signed as director (the title “director” being in her own handwriting). It appears that Fiona also signed the building contract as owner.

- The renovation works began in 2014 (a construction certificate being approved on 5 June 2014) and concluded in 2015. A final occupation certificate was issued on 13 March 2015. The cost of the renovation works was funded by Bernard and Fiona (in an amount, they contend, of over $1 million). The renovation costs were not at any time recorded in the accounts of the Company.

- The quote for the building works, dated 26 March 2014 was for $378,750 inclusive of GST. The signed contract was for a contract price of $353,500 inclusive of GST, “subject to adjustment as per contract conditions”. (As I understand it, the reduction in the price is related to the removal of joinery items and the allowance made for heating and a new floor from the contract – see T 374.39-50.) The contract provided for a deposit of $17,675 and a series of payments to be made when specified stages of the works were 95% completed. The contract provided for a number of “Prime Cost Items” (see cl 15 and item 11 of Schedule 2) which were specified as allowances and not guaranteed or lump sum amounts and where the contract contemplated that the amount expended might exceed the amount specified or conversely that part of such amounts might not be expended (containing provision as to how such amounts were to be treated). So, for example, item 11 of Schedule 2 specified the amount of $22,500 for “heating & new floor” (which items it is said were ultimately removed from the contract price).

- The largest claimed renovation expense comprises payments made to Mr Nunn’s company. At [44] of Fiona and Bernard’s written submissions, Fiona and Bernard claim that payments totalling $487,675.65 were made to Mr Nunn’s company, comprising the deposit, progress payments and other various payments pursuant to the contract of 26 March 2014. In that regard, at [122] of Fiona’s first affidavit, Fiona deposes that John Nunn issued seven variations and instructions sheets, totalling $37,029.96. (Timothy calculated that these variations, when added to the purchase price of the contract, totalled $390,029.96 – see [66] of Timothy’s submissions.) These variations were described as follows:

(a) Variation and Instruction sheet number 5 dated 5 August 2014 for $18,441.72 for additional quotation for remove entire roof/blanket.

(b) Variation and Instruction sheet number 7 dated 5 August 2014 for $1,496.00 for building/waterproofing and tiling 2 wall niches for each bathroom.

(c) Variation and Instruction sheet number 8 dated 5 August 2014 for $352.00 for installation of in wall cistern to ensuite.

(d) Variation and Instruction sheet number 10 dated 5 December 2014 for $8,129.44 for extra cost on tile to wet areas.

(e) Variation and Instruction sheet number 11 dated 5 December 2014 for $1,067.00 for strip drain to wet areas as Reece prime cost amount has been taken off contract.

(f) Variation and Instruction sheet number 12 dated 5 December 2014 for $94.60.

(g) Variation and Instruction sheet number 15 for $7,449.20 for carpet cost not quoted in building works originally.

- Fiona further deposes (at [123] of her first affidavit) that a number of variations were not recorded in written form and were paid in cash during the course of the renovations. At [126]-[128] of Fiona’s first affidavit, Fiona deposes to payments made to John Nunn totalling $226,758.16, being for less than 50% of the amount claimed for this particular contractor. In particular, Fiona deposes that the following payments were made: on 29 May 2014 - $17,675 (Invoice No. 1207); 14 July 2014 - $44,000 (Invoice No. 1220); 3 September 2014 - $33,000 (Invoice No. 1245); 17 September 2014 - $66,000 (Invoice No. 1242); 17 November 2014 - $44,000 (Invoice No. 1265); 1 February 2016 - $11,083.16 (Invoice No. 1331); 30 October 2016 - $2,000 (Invoice No. 1331); 9 September 2016 - $5,000 (Invoice No. 1331); and 26 November 2016 - $4,000 (Invoice No. 1331).

- Pausing here, I note that some payments seem to have been made before the invoice was issued by Mr Nunn’s company. For example, payment for invoice no. 1245 is purported to have been made on 3 September 2014; however, the invoice was issued by Mr Nunn’s company after that date, on 15 October 2014. I also note that Fiona deposed (at [128] of her affidavit) that Invoice No. 1265 was paid and provided proof of payment. However, Fiona deposed (at [129] of her affidavit) that there was no record to support payment of Invoice No. 1265. These issues were the subject of cross-examination and are discussed below.

- At [124]-[129] of Fiona’s first affidavit, Fiona deposes that there are no records for $268,276.20 worth of claimed payments to John Nunn. Nonetheless, Fiona deposes that she believes she has paid these claims (see at [125], [130]-[131]). These payments are as follows: 1 October 2014 - $13,788 (Invoice No. B13217); 5 October 2014 - $22,000 (Invoice No. 1244); 7 October 2014 - $970 (Invoice No. C17410); 4 November 2014 - $26,513.02 (Invoice No. 1254); 4 November 2014 - $46,963 (Invoice No. 1254); 11 November 2014 - $316.80 (Invoice No. C17548); 5 December 2014 - $44,000 (Invoice No. 1265); 11 December 2014 - $22,000 (Invoice No. 1270); 5 February 2015 - $16,825 (Invoice No. 1284); 12 March 2015 - $8,998.04 (Invoice No. 1296); 5 May 2015 - $35,576.58 (Invoice No. 1331); and 8 October 2015 - $30,325.76 (Invoice No. 1378).

Valuation as at 11 June 2015

- Mr Saunders valued the Homestead again on 11 June 2015 at $1,300,000 (the land value at $455,000 and improvements at $845 per metre), with an unfurnished rental value assessed at $600 per week.

October 2015

- By email sent on 8 October 2015, Fiona forwarded to Mr Lee copies of two valuations, saying that “both valuations have been done, please find attached. can we make sure we discuss and minute at the meeting”.

Minutes of meeting Bonny Glen Fruits – 22 October 2015

- There is in evidence a typed note that appears to be the minutes of a meeting on 22 October 2014 of Bonny Glen Fruits, recording the attendance of Mr Lee, Fiona and Timothy (though Bernard is also recorded as having contributed to the discussion at the meeting). It is not clear who prepared the minutes but they appear to have Fiona’s handwriting on at least some of the items.

- The minutes include the following item (against which it appears that Fiona recorded the word “Des”):

Caernarvon House

- Valuations of the house have been done before renovation and after. Des to contact the valuers to get true valuations. The difference between the valuations to be recorded as the expense was incurred by B&F hall personally

- Fiona’s evidence was that in 2015 Timothy was shown or sent the set of before and after valuations provided by Mr Saunders (T 103) and Fiona accepted that Timothy had said words to the effect that the valuations looked a bit overstated (although Fiona thought this was a reference to some extra outhouses that were in the post renovation valuation). Fiona seemed to accept that she had told Timothy she would have a more detailed look at the valuation but then left it to Mr Lee to get back to them about further information from the valuers (see T 104). Fiona gave evidence that she and Bernard would follow up with Mr Lee as far as wanting to put this on the company books (see T 104-105) but there appears to be nothing in writing as to this. I note that, as to the blue book, Fiona’s evidence is that words “Follow Des up 400,00” are definitely in Bernard’s writing (which Fiona assumed to be a reference to the need to follow up a facility for hail netting (T 112)).

Minutes of meeting 1 December 2015

- The typed minutes of meeting bearing this date, to which I have referred above, include the item “Des needs to supply valuations for CCC house, Tax returns and minutes. Letter stating what is required for books to be consolidated”.

- A subsequent email exchange between Fiona and Leanne Pearce indicates that both had a role in preparing minutes of meetings at least by June 2016 and that this involved communication with Mr Lee. The minutes headed Committee Meeting 3 June 2016 record the following item:

4.1 Caernarvon house improvements – Des was getting clarification from the valuers – Des forgot to do this – Des will follow this up to have a resolution by next meeting.

Discussions in relation to separation of assets

- By 2017, the brothers were involved in discussions as to the unwinding of the joint family enterprise. Timothy says that, by then, the relationship between the brothers had deteriorated (this does not appear to be disputed by Bernard and Fiona, albeit that, as noted already, they cavil with the proposition that the relationship had deteriorated as early as 2013). Bernard himself says that in 2017 his relationship was deteriorating (see at [171] of his first affidavit).

- In 2017, Bernard, Fiona and Timothy jointly engaged Mr Thornhill to “assist with their goal of separating each family from the respective jointly owned assets” (see Mr Thornhill’s email of 7 April 2017 to Mr Lee, copied to the brothers; and see Bernard’s first affidavit at [172]-[173]). Bernard deposes that there were a number of meetings at the Caernarvon cottage attended by Mr Thornhill, Timothy and Bernard, at which there was discussion as to the properties and assets.

- There was an initial meeting with Mr Thornhill on 23 March 2017 at which Bernard says that there was discussion as to the renovations and as to the valuations obtained, following which Mr Thornhill sent an email on 24 March 2017, attaching a summary of the jointly held assets and relevant details from the meeting for the brothers’ review. The list attached summarised the proposal for various assets; including that 100% of the “business” of Bonny Glen Fruits Pty Ltd would be “to Tim” but that the company might be wound up and Timothy to operate out of one of the existing companies or in a new entity; and for the assets of Caernarvon Pty Ltd (by their description this must be a reference to the Company) to be transferred to Bernard and Fiona.

- Mr Thornhill forwarded this schedule to Mr Lee by email on 7 April 2017, noting that the preferred date for the separation to be in place was 1 July 2017. Mr Lee responded by email on 13 April 2017 advising as to the steps to be followed to ascertain how a separation could be structured. Those steps included calculation of “[t]he amount owed by one party to the other on adjustment of such separation” and capital gains tax cost. There was no express reference in those emails to any reimbursement for expenses incurred in renovations of the Homestead, or any other properties. However, in evidence were undated handwritten notes apparently produced on subpoena by Mr Thornhill of a meeting with Bernard, Fiona and Timothy noting a timeframe of 1 July 2017, in which there is reference to “market value before & after reno of Caernarvon hose [sic] done. Can’t subdivide”; and that “Melrose’ includes Tim house” and the note “tim has put money into house”. The note recorded that “all agree that will value properties based on land & income producing value”.

- By 18 May 2017, the proposal in relation to jointly held assets had changed such that the business of Bonny Glen Fruits Pty Ltd was now to be to Bernard and Fiona (but with the same comments as to the possibility that the company might be wound up and that Bernard and Fiona might operate out of one of the existing companies or in a new entity).

- By 22 May 2017, it appears that there was dissension between the respective family members (see Fiona’s email to Mr Thornhill on that date referring to a meeting the previous Friday (18 May 2017) which Fiona described as “brutal and complete change around to where Tim wanted to be at the first meeting we had”). Fiona’s email to Mr Thornhill included the statement that “[s]o we are been [sic] forced to sell our much loved property. If it doesnt [sic] sell we are forced to buy out Tim which Bernard does not want to do!” (this presumably referring to a sale of the Canobolas Property including the Homestead). Mr Thornhill’s response was that he agreed that the meeting on Friday was “a total change in direction”.

- By August 2017, Mr Thornhill was conveying to the brothers his understanding that any plans to move forward with the separation of jointly owned assets had stalled and that one of the main “sticking points” was the actual and intended ownership of “Caernarvon Pty Ltd” (the owner of the Caernarvon Property) and Melrose Park (there having been communications via Fred and Pamela to the effect that their intention had been that Timothy have only 25% of Canobolas and Bernard only 25% of Melrose Park, contrary to the ASIC documents).

- A meeting took place on 4 December 2017 attended by Timothy, Bernard and Mr Thornhill, the minutes of which were prepared by Mr Thornhill. The meeting minutes included the following:

5. Residential properties on ‘Melrose’ and ‘Caernarvon’

- TH & BH agreed that there have been improvements to the residential properties on these 2 properties over time and that there may have been costs incurred by TH & BH on each of these respective properties from their own funds, and that such contribution needs to be taken into account when calculating the net asset ownership by TH & BH as part of the asset separation.

- The residential property on ‘Melrose’ is the residence of TH, and on ‘Caernarvon’ is the residence of BH

- Agreed that MT will obtain financial reports for the entities owning these properties from DL (and associated entities) to review the amounts reported in these financial reports/ balance sheet, and provide a summary to TH & BH of this financial information for further discussion as to the next steps to take to agree on the contribution made respectively by TH & BH to these properties.

- There is no reference in these meeting minutes to any existing loan agreement in relation to expenditure on renovations on the Homestead property (rather what seemed there to be recorded was that the brothers agreed at the meeting that there “may have been” costs incurred by each of them on the properties out of their own funds and that such contribution needed (in some fashion) to be taken into account when calculating the net asset ownership of the brothers as part of the asset separation).

- Fiona’s response to the minutes included (see email of 5 December 2017) that she and Bernard had done the right thing and had their house valued both before and after the renovations (and to assert that “[t]his was all agreed to by Tim and Des”).

- Bernard says that, what occurred in 2017 was that he and Timothy came to an in principle agreement that each would own his respective orchard (i.e., Canobolas and Nashdale) and that they went through a summary of assets and agreed how they would be split but that two weeks later Mr Lee advised him that Timothy did not want to split the business because he was “too sick” to take it on anymore ([183] of Bernard’s first affidavit). Bernard relies on this evidence to dispel any suggestion of recent invention.

- On 4 December 2017, Mr Thornhill recorded a meeting where the two brothers agreed that costs incurred by the others on their respective properties had to be taken into account as part of the separation (i.e., to value the assets and that there be a cash payment to “even up” the division) (see T 10). However, it seems that there was then a disagreement as to this.

- Bernard has deposed to a conversation with Timothy in around 2018 where he says that Timothy recounted their father’s opinion that the Company should be put into voluntary liquidation and the liquidators should sort out the whole thing so that “everyone gets repaid what they’re owed”; and says he agreed with this (see at [185] of Bernard’s first affidavit).

Appointment of voluntary liquidators

- In late 2018, Bernard and Timothy agreed to appoint Mr Cameron Gray and Mr Anthony Elkerton (together, the fourth respondent) as trustees for sale to realise the various properties and as provisional liquidators to realise the assets that were held by the corporate entities they controlled. Orders were made by consent to that effect on 27 November 2018 (the winding up of the companies being put on the just and equitable ground).

- Prior to the appointment of the provisional liquidators, by letter dated on 21 November 2018, solicitors acting for Bernard and Fiona (Matthews Folbigg) wrote to Timothy’s then lawyers advising that their clients’ agreement to the proposed short minutes as to the distribution of proceeds from the sale of the Caernarvon Property pending further order of the court was “not intended to dispose of” their clients’ claim that they are “entitled to an equitable claim and an adjustment against the proceeds of sale of the Caernarvon Property, in accordance with the improvements they have made to the property”. The letter stated the understanding that Bernard and Fiona had paid in excess of $600,000 from their personal funds to make improvements to the Homestead and that:

We are instructed that Tim was aware that our client’s [sic] would be undertaking this work and that any amounts spent by Fiona and Bernard on the renovations, would be recorded as an amount owed to them in the books and records of the company, however, this did not occur.

- On 12 December 2018, a report was completed by Bernard on the company activities; Bernard identified his claim and provided a copy of the (said to be contemporaneous) notes taken by Fiona of this relevant meeting, and the “before” and “after” valuations by Mr Saunders (who gave evidence in the proceeding).

Sale of properties

- The Canobolas and Nashdale Properties were sold at public auction held by the liquidators on 24 July 2019. Fiona, and an entity associated with Bernard and Fiona, together acquired the Canobolas Property. Completion of the sale was, however, delayed on at least two occasions due apparently to funding difficulties (see below).

- On 21 November 2019, Bernard’s solicitor wrote to the liquidators proposing that they grant partial vendor finance to the purchasers of the Company’s land, and other land held by the liquidators under an appointment as trustees for sale, in each case under existing contracts of sale dated 24 July 2019 to Fiona and a company associated with Bernard and Fiona. The letter proposed that Bernard’s dividend in the winding up of the Company be charged as security for the purchasers’ obligations.

- The letter of 21 November 2019 referred to discussions between the purchasers’ solicitors and the liquidators “last week” and to the need to have the “figure” of an amount to be set off under earlier orders of the Court under s 81 of the Trustee Act 1925 (NSW) (Trustee Act) in respect of the land held under the appointment as trustees for sale. Those orders had been directed to facilitating a completion of the contracts on 14 November 2019. Timothy notes that, despite the set-off permitted by those Orders in respect of the land held by the vendors under the appointment for sale as trustees, the purchasers had failed to complete; and that the letter of 21 November 2019 was there making a similar proposal in respect of Bernard’s expectation of a dividend in the winding up of the Company.

- The 21 November 2019 letter advised that it was at least desirable, if not necessary, for Bernard and Fiona to know how much they would need to raise from other lenders to pay the portion of the price not financed by the vendors (hence the need to ascertain an expected dividend).

- Timothy notes that the letter of 21 November 2019 made no reference to the proof of debt (see below) which was subsequently lodged a few days later.

Proof of debt

- On 26 November 2019, as adverted to above, Bernard and Fiona lodged a proof of debt in the liquidation of the Company, claiming as a debt the sum of $800,000 in respect of funds they claimed were expended to enlarge and renovate the Homestead between 2013 and 2015.

- The proof of debt claimed that the debt was owed by the Company pursuant to a Loan Agreement between Bernard and Fiona and the Company “for amounts advanced in relation to Caernarvon homestead improvements”. The proof of debt attached “minutes of meeting dated 16.05.2013” (being Fiona’s handwritten note – as set out earlier) and a “schedule of invoices and evidence regarding payments”. The covering letter from Bernard and Fiona’s accountant stated that the amount actually paid was $1,050,797.58 but that Bernard and Fiona were prepared to agree only to lodge a proof of debt for $800,000 in order to allow the liquidator “to have certainty regarding the amount which … Bernard may be entitled to receive as a shareholder of the company”.

Vendor Finance

- On 29 November 2019, Timothy’s solicitor received an email from the liquidators’ solicitor informing him that there was a proposal for vendor finance that one of the liquidators wished to discuss with him.

- A meeting was then held on 4 December 2019, at which Timothy’s solicitor, Mr Cakic, was informed that the proposal would require approval from the Court pursuant to s 477(2B) of the Corporations Act. On the same day, Mr Cakic made a written request for additional information. Complaint is made that this was not provided.

- On 9 December 2019, the liquidators filed an Interlocutory Process seeking approval of the vendor finance proposal pursuant to s 477(2B) of the Corporations Act. Timothy notes that the supporting affidavit of one of the liquidators, Mr Gray (affirmed on 9 December 2019) referred to the $800,000 joint proof of debt by Bernard and Fiona but did not annexe or exhibit it, nor explain its claims.

- On 10 December 2019, Timothy (whose position was that he did not have enough information to make a decision with respect to the application) sought a guarantee from the liquidators that he would receive an equivalent amount of money from the liquidation as his brother (Bernard) would receive. Timothy neither consented to nor opposed the s 477(2B) application, which was heard and determined by Rees J on 11 December 2019.

Completion of sale

- The sales of the properties were completed on or about 13 December 2019. The vendor finance was for $1.1 million. Timothy notes that the liquidator’s affidavit on the s 477(2B) application stated that he expected that all creditors would be paid and the shareholders receive distributions each exceeding $1.1 million, and that there would be no undue delay. Thus, Timothy says that the position that was being presented to Rees J was that only the shareholder dividend was treated as a material factor relied on to support the viability of the then proposed agreement. It is noted that this was mentioned as a factor in Rees J’s judgment (see p 3), her Honour’s reasons not referring to the proof of debt claim.